The expected and unexpected financial impacts of the pandemic on study abroad

Cost and affordability of study are once again top of mind in the post-COVID world

The affordability and the cost of studying abroad has always been an important consideration for international students looking to study in the main English-speaking destinations of the US, UK, Canada, Australia and New Zealand. The high cost of tuition, rising costs of living in major metropolitan centres, and unfavourable currency exchange rates make international education one of the single largest investment decisions for many families.

At the outset of the pandemic, concerns around COVID-19 cases, safety, and access to healthcare became more pressing concerns. But over time, international students have started to turn their minds back to the age-old issue of cost and affordability.

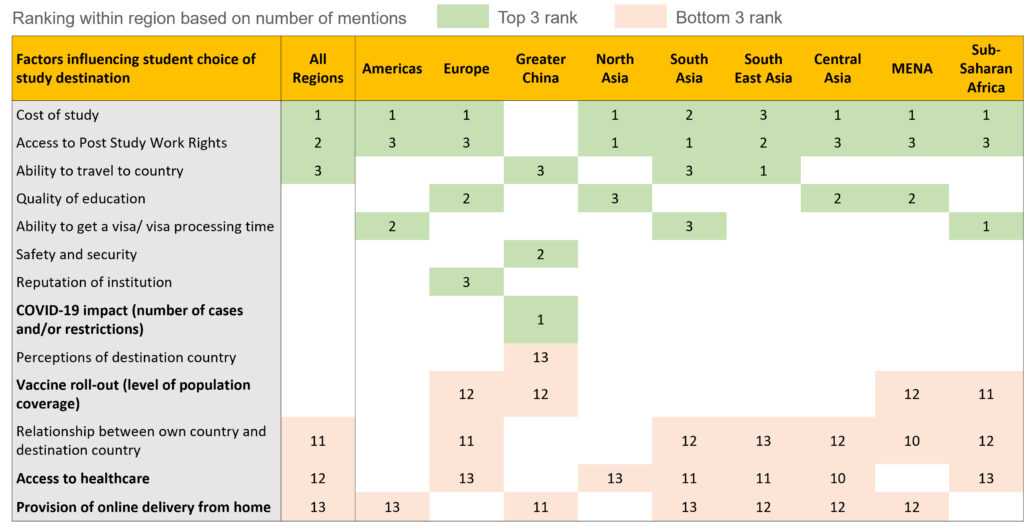

The most recent Navitas Agent Perception report found that cost of study is in fact the number one factor influencing choice of study destination across many regions. As Figure 1 shows, over 1,000 agents from around the world reflected the fact that cost of study is universally important, and in many cases, it is ranked as more important than the ability to travel or the quality of education.

Figure 1: What are currently the most important factors influencing student choice of study destination

The pandemic-induced recession has taken a financial toll on would be international students and their families, although a small proportion have benefited

For many students, parents and families, the pandemic-induced recession has undoubtedly adversely affected their ability to afford an international education experience. However, this recessionary effect is not likely to be uniform. One of the perverse consequences of the pandemic for example, is that asset-rich households have in fact prospered, while those less well-off in the service economy or the informal economy have been hardest hit.

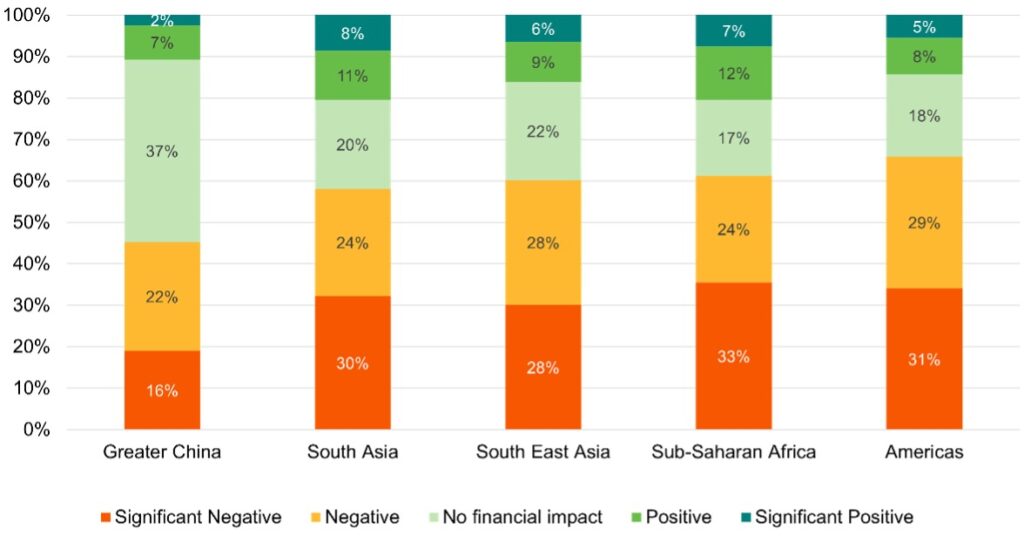

This bears out in the Navitas Agent Perception survey, which asked “Has the COVID-19 pandemic had a financial impact on your clients (students and their families)?” In response, agents reported that the majority of students and their families have experienced a negative (25%) or significant negative (28%) financial impact. On the other hand, the collective view was that about a quarter faced no financial impact (24%) while a proportion experienced a positive (9%) or significant positive impact (5%).

Figure 2 highlights the variation reported by agents between regions. In all regions the proportion of students and families negatively affected by the pandemic recession ranges from 50 to 60 per cent. On the other hand, agents also report that across most regions 15 to 20 per cent of households saw a positive or significant positive financial result. In both cases, the Greater China region is the exception, with a much larger proportion reportedly experiencing no financial impact.

Figure 2: Financial impact of the pandemic by region

A negative financial impact does not automatically mean a lower intention to study abroad

In the pre-pandemic era, the high cost of international study was often more than justified on the basis of the substantial long-term economic return on that investment. Countless studies have shown that tertiary education has a very significant impact both in terms of graduate starting salaries and lifetime earnings. For many students who choose to study abroad for want of high-quality tertiary options back home, it is a transformative experience. For those who choose to stay on to seek temporary or permanent migration, the benefits are further extended by both the experience and income gained.

We also cannot assume that a negative financial impact results in a reduced willingness to study abroad. In fact, it is reasonable to expect that those who have had a difficult time during the pandemic might be more motivated to study abroad in order to improve their circumstances. The pandemic could thus have the effect of amplifying aspirations and ambitions.

Another driver for an increased motivation to study abroad might stem from the psychological scarring of living through COVID in lockdown, without a strong government safety net, and with uncertain access to reliable healthcare. In the same way that economic security has historically been a driver for studying abroad, health security could well be a new reason for the COVID generation to pursue opportunities and life elsewhere.

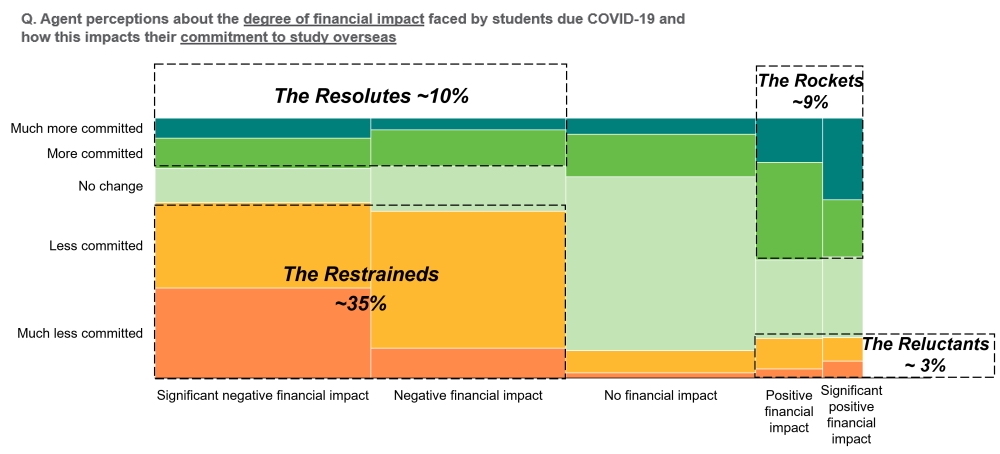

The Rockets, Reluctants, Resolutes and Restraineds

The Navitas Agent Perception survey sought to break the issue into two dimensions. First, as discussed above, what was the extent of the financial impact? But secondly, did that financial impact affect student’s commitment to study overseas? Figure 3 presents the summary result across both these questions. There are four groups of international students and families that can be seen in these results.

Figure 3: Financial impact of COVID-19 and commitment to study overseas

First, in the bottom left are the group we would most naturally associate with the pandemic. These are the group that have experienced a negative/significant negative financial impact due to the pandemic, and as a result are now less/much less committed to studying abroad. Lower financial resources naturally mean a reduced ability to meet the high costs of tuition and cost of living.

In the short-term, some of these barriers to affordability may be mitigated by improving economic conditions both at home and in the study destinations. Australia for example has become more appealing with additional work rights during and after study, severe skills shortages and low unemployment, rising wages, and the full rebate of visa application fees. While financial difficulties persist, this large group comprising 39% of would-be students are The Restrained.

“We cannot underestimate both the short and longer term impact on the capacity of some students to fund their studies. Redundancies, job losses, rising costs of travel and living expenses will have an effect on student flows and the time it takes to return to normal volumes in both source and destination countries. However, the impact will be felt differently in different markets and segments – we can expect students in India to fall into this category more than students from China for example and under-graduate students more than post-graduate.” Tony Cullen, Navitas Executive General Manager, Global Engagement.

Second, in the top left, a fair proportion of students and families that experienced negative/significant negative financial impacts due to COVID-19 are also now more/much more committed to studying abroad. The financial impact has created additional hurdles for these families, but they are undeterred; these are the 11 per cent of students that form The Resolutes.

Third, in the top right of Figure 3, there are those students and families who have seen an improvement in their financial situation and are now more/much more committed to studying overseas. We can call this group The Rockets, and they make up ~8 per cent of all students.

And finally, in the bottom right, there are those who have seen an improvement in their financial decision but are now less/much less committed to studying abroad. Despite international study becoming notionally more affordable, these students and families have likely been deterred for non-financial reasons. This group are The Reluctants, but fortunately they only make up 3 per cent of all would be international students.

In the midst of it all are the group whose commitment to study overseas has remained unchanged through the financial ups and downs of the last two years. At 40% of the prospective international student population, this group are as big as the group that are restrained.

As with so many aspects of the pandemic, the financial impact of COVID-19 has been difficult to predict. Our intuition that students are going to be mostly worse off financially and therefore much less likely to want to study abroad are likely to be overstated. The Restrained are no doubt a large proportion but there are other groups to also consider in the post-COVID recovery.